July Market Thoughts

Everything is Different Now

June Recap and July Outlook

June saw more confusion of where the micro economy in the U.S. was headed. Conflict in Iran, continued tariff confusion, and a public breakup between the richest man and the most powerful man in the world all contributed to the volatility of the news cycle.

Somewhat surprisingly, both the bond and the equity markets took headlines and data releases in stride, and both turned in positive performance.

Have investors grown tired of the overreaction from “experts”? Or is news cycle exhaustion creating a very strong case of “see you in September?”

Let's get into the data:

Inflation, as measured by CPI, rose less than expected. For the 12 months ended in May, CPI was 2.4%. The monthly number rose 0.1%.

Non-farm payrolls for June came in at 147,000. The U.S. Bureau of Labor Statistics reported that the labor market added significantly more than the 110,000 jobs that were expected, and the unemployment rate fell to 4.1%.

The U.S. dollar index has declined by more than 10%. Against a basket of other currencies, the U.S. dollar index hit a three-year low, after peaking on inauguration day.

GDP expectations were lowered. The Fed’s “dot plot” showed GDP for 2025 falling to 1.4% from 1.7% in March, and 2026 GDP expectations at 1.6% from 1.8%.

What Does the Data Add Up To?

Stable inflation and a solid labor market have likely taken interest rate cuts off the table until later in the year. Despite dire projections of the havoc tariff policy will wreak on the economy, meaningful, measurable data isn’t showing damage. Is the commentary on tariffs simply overreacting to the fear of prices, or is there more going on in the global economy than we realize? Possibly a little of both, though the economy seems to be moving on and not waiting around for the answer.

Markets are forward-looking, and tend to price in future expectations. It’s becoming normal for investors to look beyond the volatility and assume the dust will settle in their favor in the long run.

The balance of the year may be a story of volatility in the form of a “choppy” stock market that has potential to maintain momentum; a Federal Reserve that ends the year with lower rates, but takes longer to get there, and an economy that chugs along.

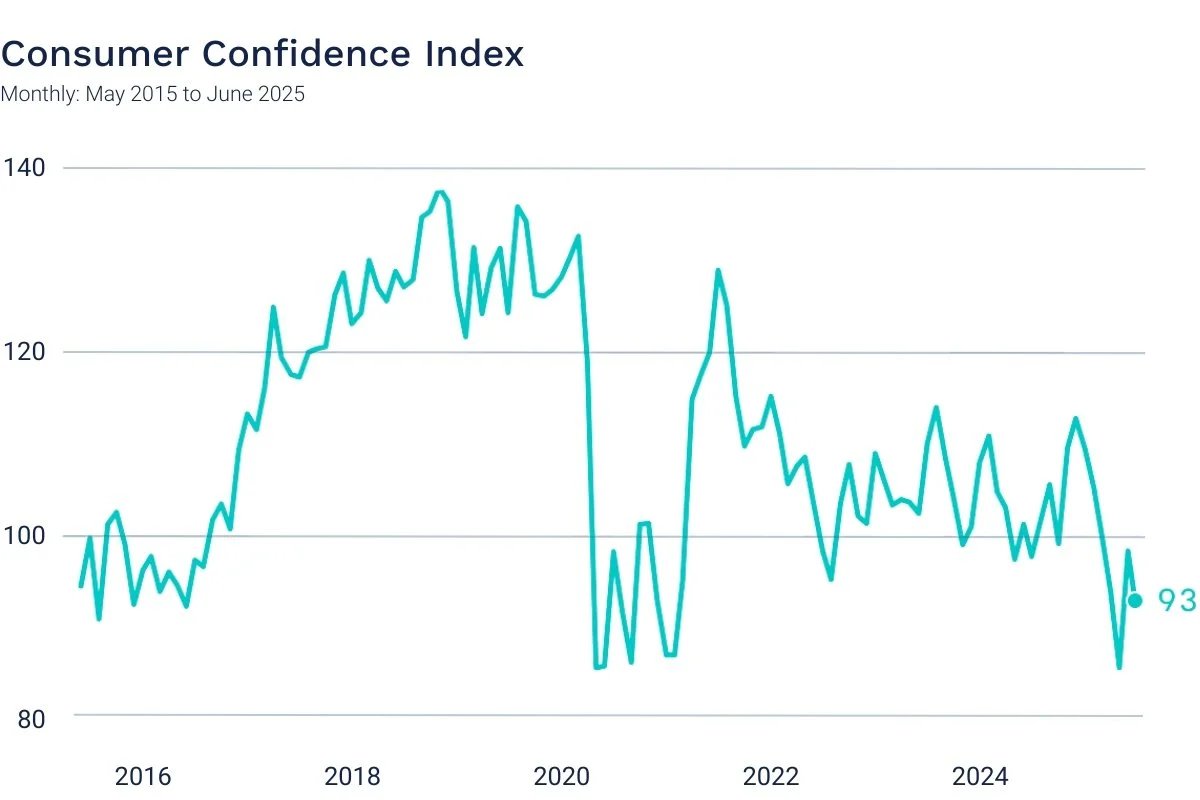

Chart of the Month: Consumer Pessimism Returns

After a “relief spike” when tariffs were rolled back in May, consumer confidence turned negative again. Consumers of all age groups cited less job availability, worse income prospects, inflation and high prices in their read of the economy.

Source: Bureau of Economic Analysis (data) Axios (visual)

Equity Markets in June

The S&P 500 was up 4.96% for the month

The Dow Jones Industrial Average gained 4.32% for the month

The S&P MidCap 400 rose 3.38% for the month

The S&P SmallCap 600 increased 3.85% for the month

Source: S&P Global. All performance as of June 30, 2025.

Nine of the eleven S&P 500 sectors had positive returns, with Information Technology maintaining the lead for the third month in a row, up 9.73% and Consumer Staples in last place, down 2.21%. The Magnificent Seven added 47% of the index return of 5.09%. Monthly intraday volatility, measured as the daily high/low, decreased again, to 0.83%, but is still historically high.

Bond Markets in June

The 10-year U.S. Treasury ended the month at a yield of 4.24%, down from 4.40% the prior month. The 30-year U.S. Treasury ended June at 4.78%, up from 4.92%. The Bloomberg U.S. Aggregate Bond Index returned 1.54%. The Bloomberg Municipal Bond Index returned 0.62%.

The Informed Investor

Planning for increased volatility in your portfolio means focusing on your own comfort level with risk. Meeting your goals isn’t just about money. The markets have been able to shrug off an escalating level of stressors and still turn in positive performance for the most part, as we hit the mid-point of the year. This can present an opportunity to rethink your investments and reposition to ensure that your risk tolerance and your portfolio investments are aligned.

Safe Lock Advisors, LLC dba Prevett Financial is an investment adviser registered in the State of Kentucky and those states in which is conducts advisory business or is exempt from registration. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. Prevett Financial has reasonable belief that this marketing does not include any false or material misleading statements or omissions of facts regarding services, investment, or client experience. Prevett Financial has reasonable belief that the content as a whole will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences. Prevett Financial has provided charts or graphs which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them.

This work is powered by Advisor I/O under the Terms of Service and may be a derivative of the original.

The information contained herein is intended to be used for educational purposes only and is not exhaustive. Diversification and/or any strategy that may be discussed does not guarantee against investment losses but are intended to help manage risk and return. If applicable, historical discussions and/or opinions are not predictive of future events. The content is presented in good faith and has been drawn from sources believed to be reliable. The content is not intended to be legal, tax or financial advice. Please consult a legal, tax or financial professional for information specific to your individual situation.

This content not reviewed by FINRA